Overview

When you first start building a product for global markets, payment collection can feel intimidating — Hong Kong bank accounts, US companies, SWIFT transfers. But once you sit down and work through it properly, it's not nearly as complicated as it looks. This guide breaks down five common SaaS payment platforms and the best withdrawal path for each.

Stripe

Stripe doesn't support Chinese bank cards, so you'll need an account from a supported country or region — Hong Kong, the US, the UK, or Singapore. Stripe supports three types of payout accounts.

1. Traditional bank accounts (checking or savings accounts)

These are accounts at regulated, brick-and-mortar banks. A checking account is a standard transaction account with little to no interest, suitable for frequent transfers. A savings account earns some interest but may have withdrawal limits. This is Stripe's most recommended payout method for stability.

2. Virtual bank accounts (e.g. Wise, Revolut, N26)

These are fintech companies operating entirely online, holding e-money licenses rather than full banking licenses. For most indie developers, the easiest option is opening a Wise account and withdrawing from Stripe to Wise, then converting to Alipay. Wise has a better reputation in the cross-border payments space than Payoneer and sees far fewer failed withdrawals. Note that Stripe does flag virtual accounts as having a higher chance of rejection — but your funds won't disappear; failed payouts are returned to your Stripe balance.

3. Instant payout debit cards

Cards like HSBC Hong Kong Visa debit or Wise Visa debit can receive funds within minutes rather than the standard 1–3 business days. However, Chinese mainland UnionPay debit cards are not supported, and fees are higher than standard payouts — not recommended for regular use.

Reference: Stripe supported bank account types · Stripe multicurrency settlement

Summary: Long-term, a traditional foreign bank account is the most stable option. If your business is just getting started and you don't want to open an overseas account yet, use Wise as a bridge and upgrade later.

Creem

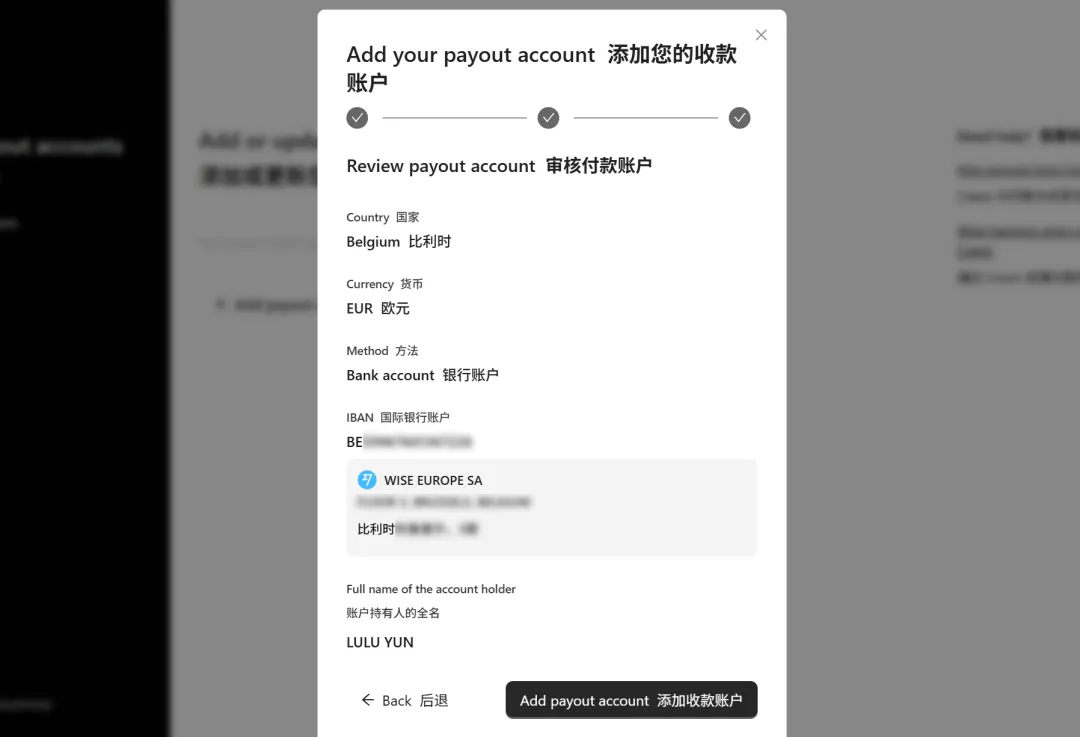

The recommended withdrawal path is: Creem → Wise EUR account → Alipay / bank card.

According to Creem's official documentation, payouts to EU/SEPA countries incur zero fees. Belgium is an EU member state, and BE-prefix IBANs fall within the SEPA zone — meaning withdrawals via Wise's Belgian IBAN are completely free.

Set your payout account here: https://www.creem.io/dashboard/balances/accounts → click Update Account.

Once configured, trigger a manual withdrawal and you're done.

Reference: Creem payout documentation

One update worth noting: Wise no longer requires an initial deposit of $20 to add USD as a currency. You can now activate USD on a zero-balance account.

PayPal

Withdrawing to a Chinese mainland bank card costs a flat $35 fee, plus currency conversion charges. Withdrawing to a Hong Kong bank account is free for amounts over HKD 1,000. If your monthly PayPal income is significant, a single trip to open a Hong Kong bank account will pay for itself quickly.

Paddle

Paddle supports both domestic and international payments and offers two payout methods.

Payoneer → Chinese bank card

Payoneer is free to apply for but has ongoing management fees. Fee structure: if the payout currency matches your local currency (e.g. receiving EUR in Europe), withdrawal is free. If there's a currency mismatch (e.g. receiving USD in China), Paddle charges either a fixed fee for smaller amounts or 1% for larger amounts. See Payoneer pricing for details.

Wire Transfer (SWIFT)

Paddle sends funds directly to your bank account via the SWIFT network. Whether fees apply depends on two factors:

- Currency match: If your bank account currency matches the payout currency (e.g. USD to a US USD account), Paddle uses local rails and charges nothing. If there's a mismatch (e.g. USD to a CNY account in China), Paddle deducts $15 from your payout before sending.

- FX conversion fee: If you ask Paddle to convert currency before paying out, Paddle reserves the right to charge up to 1.5% on the exchange rate spread.

Additionally, intermediate correspondent banks in the SWIFT chain may deduct their own fees — these are outside Paddle's control and billed to the recipient.

Recommendation: Use Payoneer for regular payouts; consider wire transfer only for large one-off amounts.

Reference: Paddle payout fees

Lemon Squeezy

Lemon Squeezy handles tax compliance automatically and supports WeChat Pay and Alipay for buyers — an advantage over Stripe for China-facing products. Two payout options are available.

Stripe Connect: Only relevant if you already have a Stripe account.

PayPal: See the PayPal section above for the most cost-effective approach.

If Lemon Squeezy allowed binding Wise or Payoneer directly, it would be a strong option — the fee structure (5% + $0.50) is the same as Paddle. For now, the choice between Lemon Squeezy and Paddle comes down to ease of onboarding and payout speed.

Reference: Lemon Squeezy getting paid

Final Thoughts

Payment infrastructure sounds complex until you map it out. The short version: open a Wise account first, use it as a bridge to start collecting revenue, and invest in a proper foreign bank account once your business gains traction. You don't need to do everything at once.